Economy:

U.S. economy accelerates to 4.1% real GDP rate in second quarter, fastest in almost 4 years - MarketWatch

The 4.1% number is an inflation adjusted number and represents the first estimate of 2nd quarter GDP growth. The estimate went over 4% due to a decline in the personal consumption inflation from the first quarter's 2.5% rate to 2.2%. Consumer spending accelerated to a 4% annual growth rate. The numbers will be revised two times over the coming weeks. News Release: Gross Domestic Product

The Atlanta Fed's GDP model estimates that the final number for the 2nd quarter will be +3.8%. GDPNow - Federal Reserve Bank of Atlanta

Trump: 'We're going to go a lot higher' than 4.1% GDP growth

Fact checking Trump’s victory lap after the second-quarter GDP report - MarketWatch

Calculated Risk: Top Twenty GDP Quarters since 2000 (prior to this release)

Existing-home sales slide for third-straight month in June, touch 5-month low as housing sputters - MarketWatch

Existing-Home Sales Subside 0.6 Percent in June | www.nar.realtor (2.2% below a year ago)

New-home sales slump in June as housing headwinds increase - MarketWatch

New Home Sales in June-Commerce Department.pdf

New Home Sales in June-Commerce Department.pdf

The U.S. Housing Market Looks Headed for Its Worst Slowdown in Years

I have predicting that home sales would likely trend down due to a number of headwinds, including prices, the rise in mortgage rates and the diminution of tax incentives as a result of "tax reform".

Last April Trump declared that trade wars are easy to win. On 7/24, Donald echoed that sentiment with the following tweet, declaring that tariffs are just great even though they are in effect a tax on those who voted for Donald:

It is possible that Trump will succeed to some measurable decree in his tariff wars. The question is whether the longer term benefits will exceed the risks to the U.S. economy when and if there is a positive outcome for the U.S.

It is possible that Trump will succeed to some measurable decree in his tariff wars. The question is whether the longer term benefits will exceed the risks to the U.S. economy when and if there is a positive outcome for the U.S.

At least the Trump meeting with the EU President Claude Juncker was a positive in that it did not blow up and both sides agreed to a cease fire for as long as negotiations are ongoing. I would call what happened a deal to avert an escalation of trade tensions-for the time being.

Juncker came well prepared for the meeting with Doofus Don, with “more than a dozen colorful cue cards with simplified explainers” about complex trade topics. Juncker’s secret weapon in trade talks with Trump: color-coded flash cards - MarketWatch Each cue card had at most 3 figures on it so that Donald would not become bored reading the card. It does not look like Juncker wanted to insult the stable genius by bringing along a coloring book.

We can probably thank the Secretary of the Treasury for restraining Donald's worst instincts, possibly by noting correctly that it would be idiotic politically to impose a 25% tariff on imported automobiles a few weeks before the November election. The EU promise to buy more soybeans and liquid natural gas will prove to be immaterial, since soybeans can be bought cheaper from non-U.S. sources and natural gas transported by pipeline is far cheaper than liquified natural gas transported by tanker across the Atlantic.

Although Trump started the tariff war with China, which resulted in China retaliating, Donald blames China rather than himself for the tariffs on U.S. farm products:

This kind of statement is for domestic purposes. Calling China "vicious" will resonate among many U.S. voters, but will not have any beneficial impact on U.S-China trade relations.

Qualcomm-NXP merger killed by China

Made in China: Trump re-election flags may get burned by his tariffs

The 4.1% number is an inflation adjusted number and represents the first estimate of 2nd quarter GDP growth. The estimate went over 4% due to a decline in the personal consumption inflation from the first quarter's 2.5% rate to 2.2%. Consumer spending accelerated to a 4% annual growth rate. The numbers will be revised two times over the coming weeks. News Release: Gross Domestic Product

The Atlanta Fed's GDP model estimates that the final number for the 2nd quarter will be +3.8%. GDPNow - Federal Reserve Bank of Atlanta

Trump: 'We're going to go a lot higher' than 4.1% GDP growth

Fact checking Trump’s victory lap after the second-quarter GDP report - MarketWatch

Calculated Risk: Top Twenty GDP Quarters since 2000 (prior to this release)

Existing-home sales slide for third-straight month in June, touch 5-month low as housing sputters - MarketWatch

Existing-Home Sales Subside 0.6 Percent in June | www.nar.realtor (2.2% below a year ago)

New-home sales slump in June as housing headwinds increase - MarketWatch

The U.S. Housing Market Looks Headed for Its Worst Slowdown in Years

I have predicting that home sales would likely trend down due to a number of headwinds, including prices, the rise in mortgage rates and the diminution of tax incentives as a result of "tax reform".

Last April Trump declared that trade wars are easy to win. On 7/24, Donald echoed that sentiment with the following tweet, declaring that tariffs are just great even though they are in effect a tax on those who voted for Donald:

At least the Trump meeting with the EU President Claude Juncker was a positive in that it did not blow up and both sides agreed to a cease fire for as long as negotiations are ongoing. I would call what happened a deal to avert an escalation of trade tensions-for the time being.

Juncker came well prepared for the meeting with Doofus Don, with “more than a dozen colorful cue cards with simplified explainers” about complex trade topics. Juncker’s secret weapon in trade talks with Trump: color-coded flash cards - MarketWatch Each cue card had at most 3 figures on it so that Donald would not become bored reading the card. It does not look like Juncker wanted to insult the stable genius by bringing along a coloring book.

We can probably thank the Secretary of the Treasury for restraining Donald's worst instincts, possibly by noting correctly that it would be idiotic politically to impose a 25% tariff on imported automobiles a few weeks before the November election. The EU promise to buy more soybeans and liquid natural gas will prove to be immaterial, since soybeans can be bought cheaper from non-U.S. sources and natural gas transported by pipeline is far cheaper than liquified natural gas transported by tanker across the Atlantic.

Although Trump started the tariff war with China, which resulted in China retaliating, Donald blames China rather than himself for the tariffs on U.S. farm products:

This kind of statement is for domestic purposes. Calling China "vicious" will resonate among many U.S. voters, but will not have any beneficial impact on U.S-China trade relations.

Qualcomm-NXP merger killed by China

Made in China: Trump re-election flags may get burned by his tariffs

Southern California home sales crash, a warning sign to the nation: CNBC

Whirlpool stock plunges as tariffs hit suppliers, steel costs: CNBC

Coke says it’s raising U.S. soda prices as metals tariffs hit can costs - MarketWatch

Trump's tariffs could derail Volvo Cars' production plans in the US, CEO warns: CNBC

How the Trump tax cut is helping to push the federal deficit to $1 trillion (corporate tax receipts as a percentage of the economy have now fallen to a 75 year low)

How the Trump tax cut is helping to push the federal deficit to $1 trillion (corporate tax receipts as a percentage of the economy have now fallen to a 75 year low)

Trump’s tax cuts are kicking a roaring economy into overdrive: Ed Yardeni - MarketWatch

Whirlpool stock plunges as tariffs hit suppliers, steel costs: CNBC

Coke says it’s raising U.S. soda prices as metals tariffs hit can costs - MarketWatch

Trump's tariffs could derail Volvo Cars' production plans in the US, CEO warns: CNBC

Trump’s tax cuts are kicking a roaring economy into overdrive: Ed Yardeni - MarketWatch

++++

Markets and Market Commentary:

Here’s what Goldman sees as the real danger trade could have on stocks - MarketWatch

It is a virtual certainty that the FED will increase the federal funds rate by .25% in September and highly probable that another .25% increase will occur in December.

Countdown to FOMC: CME FedWatch Tool

If there are two increases by year end, then the mid-point in the FF rate would be 2.375% on 12/19/18. Remember that the Federal Funds Rat is just for overnight lending. The 3 month T bill closed last Friday at a 2% yield. Daily Treasury Yield Curve Rates The investor can pick up most of 90.2% of the 2.96% ten year treasury yield in the 2.67% two year yield yield. The three year treasury yield of 2.76% is 93.24% of the ten year yield, or just another indication of a flattening yield curve.

The consensus is that Trump is trying to jawbone the FED into limiting its interest rate increases with this tweet and other statements.

I view the tweet as setting the stage for blaming others for a slowdown in the economy which is a possibility later this year. The high point in GDP growth will likely be the 2018 second quarter due in part to the tax cuts, consumers taking on more debt to fund personal consumption expenditures and increased purchases to avoid the tariffs.

I view the tweet as setting the stage for blaming others for a slowdown in the economy which is a possibility later this year. The high point in GDP growth will likely be the 2018 second quarter due in part to the tax cuts, consumers taking on more debt to fund personal consumption expenditures and increased purchases to avoid the tariffs.

Trump and the republicans will not assume any responsibility for a rise in interest rates, even though their policies have contributed to the rise in inflation that is provoking the FED to act. The last CPI report showed that inflation increased by 2.9% over the past twelve months.

The factors contributing to a rise in inflation include (1) Trump's tariffs which raise the price of imports and provided a price umbrella for domestic manufacturers to raise prices, (2) Trump's sanction on Iran that have contributed to a rise in crude oil prices, (3) the fiscal stimulus resulting from the tax cuts, and (4) a continued fiscal stimulus due to no restraint on federal spending.

David Rosenberg issues bubble warning: It will hit bull market: CNBC

ECB keeps rates unchanged amid heightened uncertainties for the global economy

UPDATE 2-Upbeat Roche bests rival Novartis as new drugs fuel growth

It is a virtual certainty that the FED will increase the federal funds rate by .25% in September and highly probable that another .25% increase will occur in December.

|

| September 2018 at 92.6% for at least a .25% increase |

|

| December 2018: 67.7% for at least two .25 increases |

If there are two increases by year end, then the mid-point in the FF rate would be 2.375% on 12/19/18. Remember that the Federal Funds Rat is just for overnight lending. The 3 month T bill closed last Friday at a 2% yield. Daily Treasury Yield Curve Rates The investor can pick up most of 90.2% of the 2.96% ten year treasury yield in the 2.67% two year yield yield. The three year treasury yield of 2.76% is 93.24% of the ten year yield, or just another indication of a flattening yield curve.

The consensus is that Trump is trying to jawbone the FED into limiting its interest rate increases with this tweet and other statements.

Trump and the republicans will not assume any responsibility for a rise in interest rates, even though their policies have contributed to the rise in inflation that is provoking the FED to act. The last CPI report showed that inflation increased by 2.9% over the past twelve months.

The factors contributing to a rise in inflation include (1) Trump's tariffs which raise the price of imports and provided a price umbrella for domestic manufacturers to raise prices, (2) Trump's sanction on Iran that have contributed to a rise in crude oil prices, (3) the fiscal stimulus resulting from the tax cuts, and (4) a continued fiscal stimulus due to no restraint on federal spending.

David Rosenberg issues bubble warning: It will hit bull market: CNBC

ECB keeps rates unchanged amid heightened uncertainties for the global economy

UPDATE 2-Upbeat Roche bests rival Novartis as new drugs fuel growth

+++

Trump:

More GOP Efforts to Undermine the Rule of Law:

In their ongoing efforts to stymie and discredit the Russia investigation, House GOP members have introduced a resolution to impeach the Deputy Attorney General Rod Rosenstein, a Republican appointed by Trump to this office.

The impeachment effort is being led by Mark Meadows (R-NC 11th) and Jim Jordan (R-Ohio 4th). House Republicans introduce articles of impeachment against Rod Rosenstein - CBS News

Other republicans joining this effort to interfere with the Russia investigation are the usual Trump sycophants:

Andy Biggs of Arizona (5th), Scott Perry of Pennsylvania (4th), Paul Gosar of Arizona (4th), Jody Hice of Georgia (10th), Matt Gaetz of Florida (1st) and Scott DesJarlais of Tennessee (4th).

None of those republicans have to worry about a backlash from constituents.

One of the impeachment counts involves Rosenstein signing off on the 4th Carter Page FISA warrant based on the bizarre and knowingly false contention that the 1st application, which Rosenstein did not sign, misled the FISA Court on the funding for the Steele memo. The baseless, shameful campaign to discredit Rod Rosenstein - The Washington Post (opinion article written by a retired federal district court judge)

Rosenstein replied that these republicans "should understand by now, the Department of Justice is not going to be extorted."

Jim Jordan is running to replace Paul Ryan as the House Speaker: Ohio Republican Rep. Jim Jordan announces bid for House Speaker He would be a good fit for the modern day GOP. Why Jim Jordan is surviving, and thriving, despite Ohio State sexual abuse scrutiny - The Washington Post

Paul Ryan, who is retiring, stated that he did not support the effort to impeach Rosenstein. Ryan opposes Rosenstein impeachment try, likely dooming it - ABC News

The number three republican in the House, Steve Scalise, supports the effort. Scalise backs impeachment for Deputy Attorney General Rosenstein in fight over Mueller documents The DOJ has turned over more than 800,000 documents to the House republicans.

The democrats in a joint statement called this republican effort a “panicked and dangerous attempt to undermine an ongoing criminal investigation in an effort to protect President Trump as the walls are closing in around him and his associates.”

+++

Important Omission in the Helsinki News Conference Transcript:

White House fails to address omission in Trump-Putin transcript - CNN

The White House omitted from the official transcript of the Helsinki this question directed to Putin and his answer:

Question: "President Putin, did you want President Trump to win the election?"

Putin Answer: "Yes, I did. Yes, I did. Because he talked about bringing the US-Russia relationship back to normal."

Putin's answer does not exist even though there is video recording it.

+++

More Trump Attacks on the Press Cheered by the Trumpsters:

Trump continued attacking the press in a speech before the Veterans of Foreign Wars national convention, which caused members to boo the press covering the event.

The VFW later apologized for their members. VFW issues apology after members 'boo' the press after Trump attack

Trump also made the following statement that is another attack on the press that is fundamentally Orwellian:

Trump: “What you’re seeing and what you’re reading is not what’s happening. Just stick with us, don’t believe the crap you see from these people, the fake news.”

People Are Comparing This Trump Quote to George Orwell | Time; TRUMP: 'Remember, what you're seeing and what you're reading is not what's happening' - YouTube

Quote from Orwell's 1984: "The Party told you to reject the evidence of your eyes and ears. It was their final, most essential command."

+++

Trump Constant Playing to His Base Rather Than Acting Like a President:

In a recent ABC poll, 51% of republicans approved of Donald casting doubt on the unanimous consensus of U.S. intelligence agencies that Russia interfered in the 2016 election. That poll may explain why Trump walked back his walk back on Russian interference. Trump has now walked back his walk-back on U.S. intelligence and Russia - The Washington Post

Trump will play to his base even when that play serves no purpose other than to throw red meat in their direction and to cause a majority to question his leadership and whether he is even capable of being authentic and truthful.

It just seems to be that Trump has become more unhinged and unmoored from reality than usual after his Helsinki news conference with Putin.

Trump and Cohen:

Cohen willing to tell Mueller that Trump knew of 2016 Russia meeting, source says: NBC; Cohen claims Trump knew in advance of 2016 Trump Tower meeting-CNN ("Cohen alleges that he was present, along with several others, when Trump was informed of the Russians' offer by Trump Jr.")

Trump has denied knowing about the meeting in advance. Don Jr. testified under oath that Donald did not know. Trump repeated his denial last Friday:

Trump disputes Cohen claim he knew of Trump Tower meeting

It is hard for me to imagine three people having less credibility. Someone else with credibility will be needed other than Cohen to testify that Donald knew about the meeting beforehand and wanted his team to meet with the Russians. That testimony could come from someone else at the meeting whose credibility is not tainted or a person who was told about the discussion by one of the participants.

Showboat Rudy Giuliani called Cohen a liar who has been lying his entire life during an interview on 7/26. On 5/6/18, Showboat Rudy said that Cohen is "an honest, honorable lawyer". Rudy Giuliani Defends Donald Trump Against Michael Cohen's Trump Tower Meeting Allegations

So Cohen secretly recorded at least one conversation with Trump.

Audio expert analyzes secret Trump-Cohen tape - CNN

Four important points that arise from the Trump-Cohen recording

How Michael Cohen’s Audio Clip Unraveled Trump’s False Statements

The recorded conversation that we know about now involved Donald reimbursing American Media Inc. for its $150,000 hush payment to playmate Karen McDougal who claimed to have a nearly year long affair with Cheating Don in 2006. Karen McDougal to Melania Trump: I’m sorry - YouTube

The affair allegedly started shortly after Melania gave birth to Barron Trump. The taped conversation occurred shortly before the 2016 election.

The Trump campaign has previously denied that Lying Don had any knowledge of the hush payment made by Trump's friend David Packer through AMI to McDougal. Donald Trump, the Playboy Model Karen McDougal, and a System for Concealing Infidelity | The New Yorker No payment was made by Donald to reimburse Packer.

The "David" referenced in the recording is most likely David Packer. The reason for buying the rights to McDougal's story, as mentioned by Donald on the tape, was in case Packer died, "hit by a truck", and the new AMI owner decided to publicly release the story. Allen Weisselberg, the chief financial officer for the Trump organization, is also mentioned on the tape. Weisselberg has reportedly been subpoenaed to testify in the Cohen probe. WSJ: Top Trump Organization official subpoenaed to testify in Michael Cohen probe - CNN

Giuliani claimed before the tape was released that Trump said "don't pay with cash". Giuliani slams 'outrageous' Cohen-Trump tape leak, claims recording ends at key point Trump clearly said "pay with cash". An audio expert concluded that Trump said "I'll pay in cash" and Cohen quickly replied "no" several times. Giuliani now claims that if the tape had not ended, the remaining conversation would be exculpatory.

When the dust clears, I believe the proof will show that no payment was made to AMI since Packer assured Cohen or Donald that he would kill the story and there was only two months left until the election. This raises a question, which is not answered by the tape, whether the AMI payment was a non-disclosed campaign contribution.

Personally, I never doubted that Donald has repeatedly cheated on his wives and that he has lied repeatedly when denying the affairs.

I had no doubt that Bill Clinton cheated on Hillary with multiple women and lied about it.

It is not much of a stretch to find that a man who cheats will lie about it until caught with proof that can not be denied without looking preposterous.

I would be shocked to find out that either Daddy Bush or Bush Jr cheated on their wives and even more shocked if Obama cheated on Michelle. That is just the way it is.

Cheating Don claims that Cohen may have broke the law when recording their conversations and once again accused the FBI of breaking into Cohen's office.

The FBI had a warrant to search Cohen's office.

The FBI had a warrant to search Cohen's office.

Trump had called the court approved search warrant "an attack on our country in a true sense" last April, which was when he first asserted the knowingly false narrative that the FBI broke into the Cohen's office.

Trump will repeat a knowingly false statement over and over again since repetition oddly makes the gullible and weak minded more likely to believe that the demonstrably false statement is true.

New York requires only one party to a conversation to consent to a recording. New York Recording Law | Digital Media Law Project The WSJ reported that the conversation happened when both parties were in NY and in the same room. There would consequently be no basis for Trump claiming that the recording was illegal.

In some states, and Tennessee would be one, a lawyer who taped a conversation without the client's consent could be disciplined but that may not be the case in NY. In other words, an act can be unethical for a lawyer without being illegal. Tennessee is also a one party consent state: Tennessee Recording Law | Digital Media Law Project.

The Special Master Barbara Jones, who reviewed the documents seized by the FBI from Cohen, had ruled that the tape was privileged.

Trump, who is complaining about the recording, waived the attorney client privilege which allows the prosecutors now to review it and possibly use it in a public manner (at trial or as part of a pleading). Trump team waived 'privilege' to release Michael Cohen's tape: Source; Trump attorneys waive privilege on secret recording about ex-Playmate payment The waiver of the privilege for that conversation could also result in an implied waiver of any other conversation on the same issue (the at-issue exception to the attorney client privilege)

++

Donald and the Evangelicals:

Donald is the candidate for white evangelicals. Trump's support among white evangelicals is currently at 77% and over 80% among Southern Baptists.

Evangelicals will still support Trump no matter how many lies he tells or how many affairs that he had during his three marriages. They deal with those moral issues by (1) believing Donald is honest and the media is lying; (2) every woman who claims to have had an extramarital affair is lying as are all of the women who claimed that Donald sexually assaulted them; and/or (3) even if some of the foregoing claims are true, and all are viewed with suspicion since they are aimed at a fellow tribe member rather than a democrat, Donald is promoting Christian values which primarily means his effort to overturn Roe v. Wade.

It can be disconcerting to listen to white Christian evangelicals voice their opinions, as they did to a reporter who wrote this article: Judgment days: In a small Alabama town, an evangelical congregation reckons with God, President Trump and the meaning of morality

I am not referring to their opinions about abortion or voting against a candidate who is pro-choice. I understand that position and would not criticize it when sincerely held which is almost invariably the case. Donald is not sincere about his current position. Pro-life voters are probably the largest single issue voters in U.S. elections.

Instead, I am referring to thoughts like (1) "Obama was acting on the behest of the Islamic nation"; (2) Obama "carried a Koran and it was not for literary purposes"; (3) God picked Donald Trump to be President; (4) Obama and Hillary were sent by Satan to rule us; (5) the time of Rosa Parks (who refused to sit in the back of a bus) was a "scary time"; (6) "we are in a religious war"; (7) "it is about the survival of the Christian nation"; (8) "I think they are trying to frame" Trump; and (9) "we are moving toward the annihilations of Christians". Warped is a far too kind of a description for those sentiments, but they are deeply and sincerely held in large swaths of America. The persons interviewed were Southern Baptists. I suspect they were on their best behavior for a WP reporter, holding back some thoughts and beliefs.

It is difficult for me to wrap my head around the idea that Donald is God's choice for President.

I am also curious about this religious war against Christians which is apparently designed to annihilate them.

When I leave my house, and drive down Franklin Road toward Brentwood, I pass 7 churches over about a 3 mile stretch and one of them looks like a small junior college. I can not see any war taking place there, but my eyes may be deceiving me. Concord Rd - Google Maps Donald did say that we can no longer believe what we see with our own eyes.

What can you say to the assertion that Donald was selected by God to be President and Obama is both a Muslim and the Anti-Christ? Generally, when speaking or listening to Trumpsters, conclusions are stated as facts and the conclusions can not be questioned with facts but only reinforced with reality creations.

Southern Baptists have a long history of being White Nationalists and Supremists. It was not until 2017 that they managed to pass a resolution denouncing White Supremacist ideology. A Resolution Against White Supremacy Causes Chaos at the Southern Baptist Convention - The Atlantic; Southern Baptist Convention Votes To Condemn White Supremacy : The Two-Way : NPR

I am reading this book on SCRIBD: The Evangelicals: The Struggle to Shape America So far, I have not read anything that I did not already know. In the First Great Awakening, the preacher Jonathan Edwards had some sermons (e.g. Sinners in the Hands of an Angry God) that reminded me of Jim Bill, the first Church of Christ preacher that I can recall. Yes we are all going to hell, fire and brimstone coming out of the ying yang.

++

Trump and Iran:

Trump threatened Iran in this all caps tirade that was in response to Iran's President saying that peace with Iran would be the mother of all peaces and a war with Iran would be the mother of all wars:

This is the exact quote that precipitated Donald's response: “America should know that peace with Iran is the mother of all peace, and war with Iran is the mother of all wars.”

This is the exact quote that precipitated Donald's response: “America should know that peace with Iran is the mother of all peace, and war with Iran is the mother of all wars.”

The Iranian Foreign Minister responded to Trump's tweet with this one:

“COLOR US UNIMPRESSED: the world heard even harsher bluster a few months ago. And Iranians have heard them — albeit more civilized ones — for forty years. We’ve been around for millennia and seen fall of empires, including our own, which lasted more than the life of some countries. BE CAUTIOUS.”

The comment from Iran's President, when viewed in its entirety by a non-mentally deranged person, would be that Iran would fight back fiercely if the U.S. launched an Iraq style invasion.

Iran warns of "countermeasures" in volley of threats after Donald Trump sends Twitter warning to Hassan Rouhani - CBS News

It looks like Donald's North Korea game plan is being applied to Iran. So what happens when another vague statement that Iran will fight if attack is made or when an actual threat is made against the U.S.? The consequences referenced by the Duck suggest nuclear annihilation would be the U.S. response.

It is possible that Donald will initiate a military conflict with Iran and then blame Iran of course for starting it.

One possible avenue for this conflict involves the ongoing U.S. effort to prevent other countries from buying Iran's oil.

If successful then Iran may attempt to block tanker traffic in the Straight of Hormuz which would disrupt oil exports to the U.S. The U.S. would then react using force to bust the blockade. Iran plans to respond in kind if U.S. blocks oil exports | Reuters

Iran responds to the military attack in a variety of non-conventional ways including terrorists attacks on U.S. soil, cyberattacks and/or other measures that do not involve a direct military confrontation with the U.S.. Who started the war in that scenario?

+++

Trump- Just Turn Everything on Its Head:

Well, what can you say other than this tweet represents a typical Trump effort to deflect deserved criticism leveled at him by making something up that has zero factual support. Lying works for Lying Don so there is no reason for him to stop. So no President has been tougher on Russia than Donald?

++++++++

Trump administration officials dismissed benefits of national monuments - The Washington Post

Canadian pot investors are being banned from entering the U.S. - CBS News (even though the investments are legal)

Why Jeff Sessions said 'lock her up' -- and why it matters - CNN (the lock her up chant continues among the Trumpsters) The Trumpster chant of course refers to Hillary and can be heard at all of Donald's rallies. It is consistent with their deeply authoritarian cores. The GOP is not a conservative party but a reactionary one with trending authoritarian tendencies.

Trump Wants to Delay Putin Meeting Until ‘After the Russia Witch Hunt’ The delay had nothing to do with the possible negative political repercussions of another meeting shortly before the November election.

++++

1. Equity REIT Common and Preferred Stock Basket Strategy:

A. Bought 100 AX.UN at C$12.9 (C$1 IB Commission):

Quote: Artis Real Estate Investment Trust (Canada: Toronto)

Closing Price Last Friday: C$12.64

Distribution: Monthly at C$.09 (C$1.08 annually)

Artis Real Estate Investment Trust Announces Monthly Cash Distribution

Yield at C$12.9 = 8.37%

Next Ex Dividend Date: 7/30/18

The same ordinary shares trade on the U.S. pink sheet exchange under the ARESF.

I recently bought 100 ARESF shares and have nothing to add to that prior discussion. Item # 1.A. $9.98 (7/9/18 Post)

B. Bought 50 DEA at $19.2 and 10 at $18.87-Used Commission Free Trades:

My commission free trades in my Schwab account will run out in a few days, so I am buying some income generating stocks that have fallen back into my buy range.

These two lots were bought in my Schwab account where my commission free trades will expire early next month.

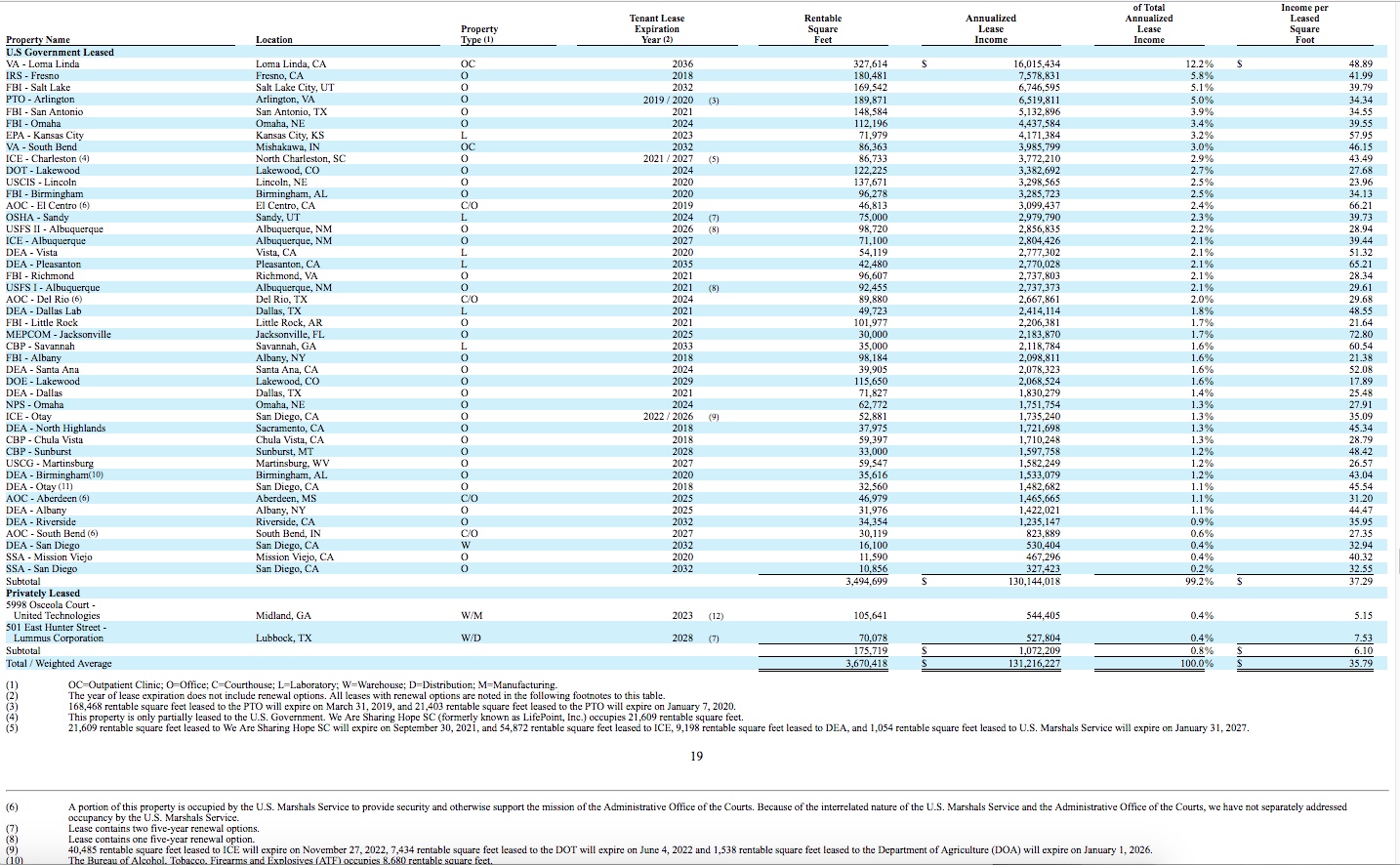

Quote: Easterly Government Properties Inc. (DEA)

Closing Price Last Friday: DEA $18.85 -$0.48 -2.48%

Website: Easterly Government Properties, Inc.

Properties as of 3/31/18:

Properties Map

SEC Filings

10-Q for the Q/E 3/31/18 (debt listed at page 10)

Dividend: Quarterly at $.26 per share

Dividends | Easterly Government Properties, Inc.

Average Cost Per Share (60 shares) = $19.143

Dividend Yield at $19.143 = 5.438%%

Last Ex Dividend Date: 6/8/18

2017 Dividend Tax Characteristics:

The ROC component reduces the tax cost basis and is not taxed as a dividend. Since none of the dividend is classified as qualified, it is at least possible to turn the ROC dividend component into a long term capital gain which would be better than the highest marginal tax rate for ordinary income for higher income taxpayers. ROC classification is irrelevant in a U.S. retirement account.

The ROC component reduces the tax cost basis and is not taxed as a dividend. Since none of the dividend is classified as qualified, it is at least possible to turn the ROC dividend component into a long term capital gain which would be better than the highest marginal tax rate for ordinary income for higher income taxpayers. ROC classification is irrelevant in a U.S. retirement account.

For an equity REIT's dividend, ROC is created by the dividend exceeding GAAP net income.

Prior Trades:

Item 1.D. Sold 10 DEA at $21.44-Used Commission Free Trade (5/17/18 Post)(profit snapshot = $22.59)-Item # 1.A. Bought 10 DEA at $19.18 (3/8/18 Post)

Item 5. A. Sold 50 DEA at $21.59-Used Commission Free Trade (12/11/17 Post)(profit snapshot =$97.85)-Item # 3.A. Bought 50 DEA $19.64 (8/19/17 Post)

This is small ball within the Equity REIT basket strategy.

Last Earnings Report: Easterly Government Properties Reports First Quarter 2018 Results

Unlike most equity REITs, DEA makes what I would consider a proper disclosure of free cash flow.

Personally, I view most reports as providing inadequate free cash flow numbers, meaning basically cash that is available for distribution.

Only a few REITs breakout routine maintenance expenditures as a deduction from FFO to arrive at FAD for example. Money spent to maintain the property is not cash available for distribution

DEA makes adjustments to funds from operation that provide a better picture of funds available for distribution ("FAD") compared to most other REITs. The result is that DEA's FAD number is not comparable to other REITs that fail to make those adjustments.

DEA reported FFO per share at $.31 which appears to provide good coverage for the quarterly dividend. The company then adjusts that number down to a AFFO of $.26 per share. One of the adjustments is to remove non-cash revenue created by the straight line rent accounting convention.

DEA then calculates cash available for distribution which comes to $.221 per share. Among the cash expenditures deducted from the AFFO number are "acquisition costs", "maintenance capital expenditures", "contractual tenant improvements" and "leasing related expenditures".

For this quarter, the dividend is not covered by FAD but was covered by AFFO and FFO. Some deductions from the AFFO calculation to arrive at FAD were materially larger in the 2018 first quarter compared to the 2017 first quarter.

Debt:

Sourced: Pages 23-24 10-Q for the Q/E 3/31/18

Recent News Since Last Discussion:

Easterly Government Properties Completes Acquisition of 90,085 SF Department of Veterans Affairs Outpatient Facility in San Jose, California

Easterly Government Properties Announces Pricing of Common Stock Offering (6/19/18 Press Release)(public offering price was at $19.25); Prospectus

Prior to that stock offering, DEA sold 4.3M shares, plus the greenshoe, at $19 back in March 2017: Prospectus

The initial public offering was in February 2015 at $15 per share. Prospectus

Note that DEA also has an ATM program: Prospectus

C. Bought 10 DEA at $18.88-Used Fidelity Commission Free Trade:

This starts a small ball buying program in this account. Each subsequent purchase has to be a the lowest price in the chain. I have an abundance of free trades in this account that expire in 2020.

More GOP Efforts to Undermine the Rule of Law:

In their ongoing efforts to stymie and discredit the Russia investigation, House GOP members have introduced a resolution to impeach the Deputy Attorney General Rod Rosenstein, a Republican appointed by Trump to this office.

The impeachment effort is being led by Mark Meadows (R-NC 11th) and Jim Jordan (R-Ohio 4th). House Republicans introduce articles of impeachment against Rod Rosenstein - CBS News

Other republicans joining this effort to interfere with the Russia investigation are the usual Trump sycophants:

Andy Biggs of Arizona (5th), Scott Perry of Pennsylvania (4th), Paul Gosar of Arizona (4th), Jody Hice of Georgia (10th), Matt Gaetz of Florida (1st) and Scott DesJarlais of Tennessee (4th).

None of those republicans have to worry about a backlash from constituents.

One of the impeachment counts involves Rosenstein signing off on the 4th Carter Page FISA warrant based on the bizarre and knowingly false contention that the 1st application, which Rosenstein did not sign, misled the FISA Court on the funding for the Steele memo. The baseless, shameful campaign to discredit Rod Rosenstein - The Washington Post (opinion article written by a retired federal district court judge)

Rosenstein replied that these republicans "should understand by now, the Department of Justice is not going to be extorted."

Jim Jordan is running to replace Paul Ryan as the House Speaker: Ohio Republican Rep. Jim Jordan announces bid for House Speaker He would be a good fit for the modern day GOP. Why Jim Jordan is surviving, and thriving, despite Ohio State sexual abuse scrutiny - The Washington Post

Paul Ryan, who is retiring, stated that he did not support the effort to impeach Rosenstein. Ryan opposes Rosenstein impeachment try, likely dooming it - ABC News

The number three republican in the House, Steve Scalise, supports the effort. Scalise backs impeachment for Deputy Attorney General Rosenstein in fight over Mueller documents The DOJ has turned over more than 800,000 documents to the House republicans.

The democrats in a joint statement called this republican effort a “panicked and dangerous attempt to undermine an ongoing criminal investigation in an effort to protect President Trump as the walls are closing in around him and his associates.”

+++

Important Omission in the Helsinki News Conference Transcript:

White House fails to address omission in Trump-Putin transcript - CNN

The White House omitted from the official transcript of the Helsinki this question directed to Putin and his answer:

Question: "President Putin, did you want President Trump to win the election?"

Putin Answer: "Yes, I did. Yes, I did. Because he talked about bringing the US-Russia relationship back to normal."

Putin's answer does not exist even though there is video recording it.

+++

More Trump Attacks on the Press Cheered by the Trumpsters:

Trump continued attacking the press in a speech before the Veterans of Foreign Wars national convention, which caused members to boo the press covering the event.

The VFW later apologized for their members. VFW issues apology after members 'boo' the press after Trump attack

Trump also made the following statement that is another attack on the press that is fundamentally Orwellian:

Trump: “What you’re seeing and what you’re reading is not what’s happening. Just stick with us, don’t believe the crap you see from these people, the fake news.”

People Are Comparing This Trump Quote to George Orwell | Time; TRUMP: 'Remember, what you're seeing and what you're reading is not what's happening' - YouTube

Quote from Orwell's 1984: "The Party told you to reject the evidence of your eyes and ears. It was their final, most essential command."

+++

Trump Constant Playing to His Base Rather Than Acting Like a President:

In a recent ABC poll, 51% of republicans approved of Donald casting doubt on the unanimous consensus of U.S. intelligence agencies that Russia interfered in the 2016 election. That poll may explain why Trump walked back his walk back on Russian interference. Trump has now walked back his walk-back on U.S. intelligence and Russia - The Washington Post

Trump will play to his base even when that play serves no purpose other than to throw red meat in their direction and to cause a majority to question his leadership and whether he is even capable of being authentic and truthful.

It just seems to be that Trump has become more unhinged and unmoored from reality than usual after his Helsinki news conference with Putin.

Trump and Cohen:

Cohen willing to tell Mueller that Trump knew of 2016 Russia meeting, source says: NBC; Cohen claims Trump knew in advance of 2016 Trump Tower meeting-CNN ("Cohen alleges that he was present, along with several others, when Trump was informed of the Russians' offer by Trump Jr.")

Trump has denied knowing about the meeting in advance. Don Jr. testified under oath that Donald did not know. Trump repeated his denial last Friday:

Trump disputes Cohen claim he knew of Trump Tower meeting

It is hard for me to imagine three people having less credibility. Someone else with credibility will be needed other than Cohen to testify that Donald knew about the meeting beforehand and wanted his team to meet with the Russians. That testimony could come from someone else at the meeting whose credibility is not tainted or a person who was told about the discussion by one of the participants.

Showboat Rudy Giuliani called Cohen a liar who has been lying his entire life during an interview on 7/26. On 5/6/18, Showboat Rudy said that Cohen is "an honest, honorable lawyer". Rudy Giuliani Defends Donald Trump Against Michael Cohen's Trump Tower Meeting Allegations

So Cohen secretly recorded at least one conversation with Trump.

Audio expert analyzes secret Trump-Cohen tape - CNN

Four important points that arise from the Trump-Cohen recording

How Michael Cohen’s Audio Clip Unraveled Trump’s False Statements

The recorded conversation that we know about now involved Donald reimbursing American Media Inc. for its $150,000 hush payment to playmate Karen McDougal who claimed to have a nearly year long affair with Cheating Don in 2006. Karen McDougal to Melania Trump: I’m sorry - YouTube

The affair allegedly started shortly after Melania gave birth to Barron Trump. The taped conversation occurred shortly before the 2016 election.

The Trump campaign has previously denied that Lying Don had any knowledge of the hush payment made by Trump's friend David Packer through AMI to McDougal. Donald Trump, the Playboy Model Karen McDougal, and a System for Concealing Infidelity | The New Yorker No payment was made by Donald to reimburse Packer.

The "David" referenced in the recording is most likely David Packer. The reason for buying the rights to McDougal's story, as mentioned by Donald on the tape, was in case Packer died, "hit by a truck", and the new AMI owner decided to publicly release the story. Allen Weisselberg, the chief financial officer for the Trump organization, is also mentioned on the tape. Weisselberg has reportedly been subpoenaed to testify in the Cohen probe. WSJ: Top Trump Organization official subpoenaed to testify in Michael Cohen probe - CNN

Giuliani claimed before the tape was released that Trump said "don't pay with cash". Giuliani slams 'outrageous' Cohen-Trump tape leak, claims recording ends at key point Trump clearly said "pay with cash". An audio expert concluded that Trump said "I'll pay in cash" and Cohen quickly replied "no" several times. Giuliani now claims that if the tape had not ended, the remaining conversation would be exculpatory.

When the dust clears, I believe the proof will show that no payment was made to AMI since Packer assured Cohen or Donald that he would kill the story and there was only two months left until the election. This raises a question, which is not answered by the tape, whether the AMI payment was a non-disclosed campaign contribution.

Personally, I never doubted that Donald has repeatedly cheated on his wives and that he has lied repeatedly when denying the affairs.

I had no doubt that Bill Clinton cheated on Hillary with multiple women and lied about it.

It is not much of a stretch to find that a man who cheats will lie about it until caught with proof that can not be denied without looking preposterous.

I would be shocked to find out that either Daddy Bush or Bush Jr cheated on their wives and even more shocked if Obama cheated on Michelle. That is just the way it is.

Cheating Don claims that Cohen may have broke the law when recording their conversations and once again accused the FBI of breaking into Cohen's office.

Trump had called the court approved search warrant "an attack on our country in a true sense" last April, which was when he first asserted the knowingly false narrative that the FBI broke into the Cohen's office.

Trump will repeat a knowingly false statement over and over again since repetition oddly makes the gullible and weak minded more likely to believe that the demonstrably false statement is true.

New York requires only one party to a conversation to consent to a recording. New York Recording Law | Digital Media Law Project The WSJ reported that the conversation happened when both parties were in NY and in the same room. There would consequently be no basis for Trump claiming that the recording was illegal.

In some states, and Tennessee would be one, a lawyer who taped a conversation without the client's consent could be disciplined but that may not be the case in NY. In other words, an act can be unethical for a lawyer without being illegal. Tennessee is also a one party consent state: Tennessee Recording Law | Digital Media Law Project.

The Special Master Barbara Jones, who reviewed the documents seized by the FBI from Cohen, had ruled that the tape was privileged.

Trump, who is complaining about the recording, waived the attorney client privilege which allows the prosecutors now to review it and possibly use it in a public manner (at trial or as part of a pleading). Trump team waived 'privilege' to release Michael Cohen's tape: Source; Trump attorneys waive privilege on secret recording about ex-Playmate payment The waiver of the privilege for that conversation could also result in an implied waiver of any other conversation on the same issue (the at-issue exception to the attorney client privilege)

++

Donald and the Evangelicals:

Donald is the candidate for white evangelicals. Trump's support among white evangelicals is currently at 77% and over 80% among Southern Baptists.

Evangelicals will still support Trump no matter how many lies he tells or how many affairs that he had during his three marriages. They deal with those moral issues by (1) believing Donald is honest and the media is lying; (2) every woman who claims to have had an extramarital affair is lying as are all of the women who claimed that Donald sexually assaulted them; and/or (3) even if some of the foregoing claims are true, and all are viewed with suspicion since they are aimed at a fellow tribe member rather than a democrat, Donald is promoting Christian values which primarily means his effort to overturn Roe v. Wade.

It can be disconcerting to listen to white Christian evangelicals voice their opinions, as they did to a reporter who wrote this article: Judgment days: In a small Alabama town, an evangelical congregation reckons with God, President Trump and the meaning of morality

I am not referring to their opinions about abortion or voting against a candidate who is pro-choice. I understand that position and would not criticize it when sincerely held which is almost invariably the case. Donald is not sincere about his current position. Pro-life voters are probably the largest single issue voters in U.S. elections.

Instead, I am referring to thoughts like (1) "Obama was acting on the behest of the Islamic nation"; (2) Obama "carried a Koran and it was not for literary purposes"; (3) God picked Donald Trump to be President; (4) Obama and Hillary were sent by Satan to rule us; (5) the time of Rosa Parks (who refused to sit in the back of a bus) was a "scary time"; (6) "we are in a religious war"; (7) "it is about the survival of the Christian nation"; (8) "I think they are trying to frame" Trump; and (9) "we are moving toward the annihilations of Christians". Warped is a far too kind of a description for those sentiments, but they are deeply and sincerely held in large swaths of America. The persons interviewed were Southern Baptists. I suspect they were on their best behavior for a WP reporter, holding back some thoughts and beliefs.

It is difficult for me to wrap my head around the idea that Donald is God's choice for President.

I am also curious about this religious war against Christians which is apparently designed to annihilate them.

When I leave my house, and drive down Franklin Road toward Brentwood, I pass 7 churches over about a 3 mile stretch and one of them looks like a small junior college. I can not see any war taking place there, but my eyes may be deceiving me. Concord Rd - Google Maps Donald did say that we can no longer believe what we see with our own eyes.

What can you say to the assertion that Donald was selected by God to be President and Obama is both a Muslim and the Anti-Christ? Generally, when speaking or listening to Trumpsters, conclusions are stated as facts and the conclusions can not be questioned with facts but only reinforced with reality creations.

Southern Baptists have a long history of being White Nationalists and Supremists. It was not until 2017 that they managed to pass a resolution denouncing White Supremacist ideology. A Resolution Against White Supremacy Causes Chaos at the Southern Baptist Convention - The Atlantic; Southern Baptist Convention Votes To Condemn White Supremacy : The Two-Way : NPR

I am reading this book on SCRIBD: The Evangelicals: The Struggle to Shape America So far, I have not read anything that I did not already know. In the First Great Awakening, the preacher Jonathan Edwards had some sermons (e.g. Sinners in the Hands of an Angry God) that reminded me of Jim Bill, the first Church of Christ preacher that I can recall. Yes we are all going to hell, fire and brimstone coming out of the ying yang.

Trump and Iran:

Trump threatened Iran in this all caps tirade that was in response to Iran's President saying that peace with Iran would be the mother of all peaces and a war with Iran would be the mother of all wars:

The Iranian Foreign Minister responded to Trump's tweet with this one:

“COLOR US UNIMPRESSED: the world heard even harsher bluster a few months ago. And Iranians have heard them — albeit more civilized ones — for forty years. We’ve been around for millennia and seen fall of empires, including our own, which lasted more than the life of some countries. BE CAUTIOUS.”

The comment from Iran's President, when viewed in its entirety by a non-mentally deranged person, would be that Iran would fight back fiercely if the U.S. launched an Iraq style invasion.

Iran warns of "countermeasures" in volley of threats after Donald Trump sends Twitter warning to Hassan Rouhani - CBS News

It looks like Donald's North Korea game plan is being applied to Iran. So what happens when another vague statement that Iran will fight if attack is made or when an actual threat is made against the U.S.? The consequences referenced by the Duck suggest nuclear annihilation would be the U.S. response.

It is possible that Donald will initiate a military conflict with Iran and then blame Iran of course for starting it.

One possible avenue for this conflict involves the ongoing U.S. effort to prevent other countries from buying Iran's oil.

If successful then Iran may attempt to block tanker traffic in the Straight of Hormuz which would disrupt oil exports to the U.S. The U.S. would then react using force to bust the blockade. Iran plans to respond in kind if U.S. blocks oil exports | Reuters

Iran responds to the military attack in a variety of non-conventional ways including terrorists attacks on U.S. soil, cyberattacks and/or other measures that do not involve a direct military confrontation with the U.S.. Who started the war in that scenario?

+++

Trump- Just Turn Everything on Its Head:

Well, what can you say other than this tweet represents a typical Trump effort to deflect deserved criticism leveled at him by making something up that has zero factual support. Lying works for Lying Don so there is no reason for him to stop. So no President has been tougher on Russia than Donald?

++++++++

Trump administration officials dismissed benefits of national monuments - The Washington Post

Canadian pot investors are being banned from entering the U.S. - CBS News (even though the investments are legal)

Why Jeff Sessions said 'lock her up' -- and why it matters - CNN (the lock her up chant continues among the Trumpsters) The Trumpster chant of course refers to Hillary and can be heard at all of Donald's rallies. It is consistent with their deeply authoritarian cores. The GOP is not a conservative party but a reactionary one with trending authoritarian tendencies.

Trump Wants to Delay Putin Meeting Until ‘After the Russia Witch Hunt’ The delay had nothing to do with the possible negative political repercussions of another meeting shortly before the November election.

++++

1. Equity REIT Common and Preferred Stock Basket Strategy:

A. Bought 100 AX.UN at C$12.9 (C$1 IB Commission):

Quote: Artis Real Estate Investment Trust (Canada: Toronto)

Closing Price Last Friday: C$12.64

Distribution: Monthly at C$.09 (C$1.08 annually)

Artis Real Estate Investment Trust Announces Monthly Cash Distribution

Yield at C$12.9 = 8.37%

Next Ex Dividend Date: 7/30/18

The same ordinary shares trade on the U.S. pink sheet exchange under the ARESF.

I recently bought 100 ARESF shares and have nothing to add to that prior discussion. Item # 1.A. $9.98 (7/9/18 Post)

B. Bought 50 DEA at $19.2 and 10 at $18.87-Used Commission Free Trades:

|

| 2 Year History This Account |

These two lots were bought in my Schwab account where my commission free trades will expire early next month.

Quote: Easterly Government Properties Inc. (DEA)

Closing Price Last Friday: DEA $18.85 -$0.48 -2.48%

Website: Easterly Government Properties, Inc.

Properties as of 3/31/18:

Properties Map

SEC Filings

10-Q for the Q/E 3/31/18 (debt listed at page 10)

Dividend: Quarterly at $.26 per share

Dividends | Easterly Government Properties, Inc.

Average Cost Per Share (60 shares) = $19.143

Dividend Yield at $19.143 = 5.438%%

Last Ex Dividend Date: 6/8/18

2017 Dividend Tax Characteristics:

For an equity REIT's dividend, ROC is created by the dividend exceeding GAAP net income.

Prior Trades:

Item 1.D. Sold 10 DEA at $21.44-Used Commission Free Trade (5/17/18 Post)(profit snapshot = $22.59)-Item # 1.A. Bought 10 DEA at $19.18 (3/8/18 Post)

Item 5. A. Sold 50 DEA at $21.59-Used Commission Free Trade (12/11/17 Post)(profit snapshot =$97.85)-Item # 3.A. Bought 50 DEA $19.64 (8/19/17 Post)

This is small ball within the Equity REIT basket strategy.

Last Earnings Report: Easterly Government Properties Reports First Quarter 2018 Results

Unlike most equity REITs, DEA makes what I would consider a proper disclosure of free cash flow.

Personally, I view most reports as providing inadequate free cash flow numbers, meaning basically cash that is available for distribution.

Only a few REITs breakout routine maintenance expenditures as a deduction from FFO to arrive at FAD for example. Money spent to maintain the property is not cash available for distribution

DEA makes adjustments to funds from operation that provide a better picture of funds available for distribution ("FAD") compared to most other REITs. The result is that DEA's FAD number is not comparable to other REITs that fail to make those adjustments.

DEA reported FFO per share at $.31 which appears to provide good coverage for the quarterly dividend. The company then adjusts that number down to a AFFO of $.26 per share. One of the adjustments is to remove non-cash revenue created by the straight line rent accounting convention.

DEA then calculates cash available for distribution which comes to $.221 per share. Among the cash expenditures deducted from the AFFO number are "acquisition costs", "maintenance capital expenditures", "contractual tenant improvements" and "leasing related expenditures".

For this quarter, the dividend is not covered by FAD but was covered by AFFO and FFO. Some deductions from the AFFO calculation to arrive at FAD were materially larger in the 2018 first quarter compared to the 2017 first quarter.

Debt:

Sourced: Pages 23-24 10-Q for the Q/E 3/31/18

Recent News Since Last Discussion:

Easterly Government Properties Completes Acquisition of 90,085 SF Department of Veterans Affairs Outpatient Facility in San Jose, California

Easterly Government Properties Announces Pricing of Common Stock Offering (6/19/18 Press Release)(public offering price was at $19.25); Prospectus

Prior to that stock offering, DEA sold 4.3M shares, plus the greenshoe, at $19 back in March 2017: Prospectus

The initial public offering was in February 2015 at $15 per share. Prospectus

Note that DEA also has an ATM program: Prospectus

C. Bought 10 DEA at $18.88-Used Fidelity Commission Free Trade:

This starts a small ball buying program in this account. Each subsequent purchase has to be a the lowest price in the chain. I have an abundance of free trades in this account that expire in 2020.

2. Income Generation-BDCs:

A. Bought 50 SLRC at $20.82-Used Commission Free Trade:

Quote: Solar Capital Ltd. (SLRC)

Solar Capital Filings with the SEC

Closing Price Last Friday: SLRC $21.19 +$0.36 +1.73%

Website: Home

2017 Annual Report Form 10-K (discussion of risk factors starts at page 24 and ends at page 52)

The simple goal for any BDC purchase is to collect some dividends and to escape with whatever profit is available.

SLRC Interactive Stock Chart:

Current Dividend: Quarterly at $.41 per share

The quarterly dividend was cut from $.6 to $.4 per share in 2013. This occurred after received $237M in proceeds after monetizing three investments. News Release

Dividend Yield at $20.82 = 7.877%

2017 Dividend Tax Treatment: No part of the dividend was characterized as qualified:

Prior Discussions:

Item # 2 Bought 50 SLRC at $18.38 (11/24/14)

I sold that lot for a $18.95 profit and then bought the lot back at $16.77: Item # 1 Update For Portfolio Positioning And Management As Of 10/1/15 - South Gent | Seeking Alpha

I discussed selling that lot for a $43.98 profit after receiving one quarterly dividend in this post: Update For Portfolio Positioning And Management As Of 3/13/16 - South Gent | Seeking Alpha I would have been better off keeping it.

Net Asset Value Per Share History: Stable for a BDC

Sourced from 10-Q Filings

3/31/18: $21.87

9/30/17: $21.80

9/30/16: $21.72

9/30/15: $21.52

9/30/14: $22.34

9/30/13: $22.25

9/30/12: $22.7

9/30/11: $21.2

3/31/2010: $22.18 (first 10-Q)

Initial Public Offering February 2010: Prospectus (priced at $18.5 to the public and $17.205 to the underwriters)

Public Stock Offerings:

In January 2013, the company priced a common stock offering to the public at $24.4 per share: Prospectus Supplement, see also discussion at pages 76-77 in 2017 Form 10-K.

I view it as a positive that this BDC has avoided a stock offering since January 2013. Most externally managed BDCs have repeatedly sold stock at below net asset value per share.

Earnings Report for the Q/E 3/31/18:

Solar Capital Ltd. Announces Quarter Ended March 31, 2018 Financial Results; Net Investment Income Per Share of $0.45; Declares Quarterly Distribution of $0.41 Per Share for Q2, 2018

"At March 31, 2018, 98.2% of the Company’s Comprehensive Investment Portfolio was invested in senior secured loans, comprised of 78.9% first lien senior secured loans and approximately 19.3% second lien senior secured loans. Year over year, second lien loan exposure of the Comprehensive Investment Portfolio declined by approximately 40%, as the Company has focused its origination efforts on underwriting first lien and stretch first lien loans to upper middle market sponsor-owned companies as well as commercial finance investments." (emphasis added)

Note that 80.5% of the investments are in floating rate loans.

Note that 80.5% of the investments are in floating rate loans.

"As a reminder, the Company’s Board of Directors recently approved a voluntary 25 basis point permanent reduction in the investment advisor’s management fee, effective January 1, 2018."

SLRC Senior Unsecured Bonds:

I have also traded a SLRC senior unsecured bond that was called early by the company at its $25 par value. South Gent's Comment Blog # 6: Bought 50 SLRA at $24.45. I allowed the issuer to redeem my position at par plus accrued and unpaid interest which occurred in 1 partial call and than a full call.

Solar Capital Ltd. to Redeem Remaining $75 Million of 6.75% Senior Unsecured Notes due 2042; Increases Expected 2018 Net Investment Income by $0.04 Per Share; Prospectus Supplement

That bond was replaced with a $1K par value 4.5% senior unsecured bond maturing in 2023: Solar Capital Ltd. Prices Public Offering of $75 Million 4.50% Notes Due 2023

A. Bought 50 SLRC at $20.82-Used Commission Free Trade:

Quote: Solar Capital Ltd. (SLRC)

Solar Capital Filings with the SEC

Closing Price Last Friday: SLRC $21.19 +$0.36 +1.73%

Website: Home

2017 Annual Report Form 10-K (discussion of risk factors starts at page 24 and ends at page 52)

The simple goal for any BDC purchase is to collect some dividends and to escape with whatever profit is available.

SLRC Interactive Stock Chart:

Current Dividend: Quarterly at $.41 per share

The quarterly dividend was cut from $.6 to $.4 per share in 2013. This occurred after received $237M in proceeds after monetizing three investments. News Release

Dividend Yield at $20.82 = 7.877%

2017 Dividend Tax Treatment: No part of the dividend was characterized as qualified:

Prior Discussions:

Item # 2 Bought 50 SLRC at $18.38 (11/24/14)

I sold that lot for a $18.95 profit and then bought the lot back at $16.77: Item # 1 Update For Portfolio Positioning And Management As Of 10/1/15 - South Gent | Seeking Alpha

I discussed selling that lot for a $43.98 profit after receiving one quarterly dividend in this post: Update For Portfolio Positioning And Management As Of 3/13/16 - South Gent | Seeking Alpha I would have been better off keeping it.

Net Asset Value Per Share History: Stable for a BDC

Sourced from 10-Q Filings

3/31/18: $21.87

9/30/17: $21.80

9/30/16: $21.72

9/30/15: $21.52

9/30/14: $22.34

9/30/13: $22.25

9/30/12: $22.7

9/30/11: $21.2

3/31/2010: $22.18 (first 10-Q)

Initial Public Offering February 2010: Prospectus (priced at $18.5 to the public and $17.205 to the underwriters)

Public Stock Offerings:

In January 2013, the company priced a common stock offering to the public at $24.4 per share: Prospectus Supplement, see also discussion at pages 76-77 in 2017 Form 10-K.

I view it as a positive that this BDC has avoided a stock offering since January 2013. Most externally managed BDCs have repeatedly sold stock at below net asset value per share.

Earnings Report for the Q/E 3/31/18:

Solar Capital Ltd. Announces Quarter Ended March 31, 2018 Financial Results; Net Investment Income Per Share of $0.45; Declares Quarterly Distribution of $0.41 Per Share for Q2, 2018

"At March 31, 2018, 98.2% of the Company’s Comprehensive Investment Portfolio was invested in senior secured loans, comprised of 78.9% first lien senior secured loans and approximately 19.3% second lien senior secured loans. Year over year, second lien loan exposure of the Comprehensive Investment Portfolio declined by approximately 40%, as the Company has focused its origination efforts on underwriting first lien and stretch first lien loans to upper middle market sponsor-owned companies as well as commercial finance investments." (emphasis added)

"As a reminder, the Company’s Board of Directors recently approved a voluntary 25 basis point permanent reduction in the investment advisor’s management fee, effective January 1, 2018."

SLRC Senior Unsecured Bonds:

I have also traded a SLRC senior unsecured bond that was called early by the company at its $25 par value. South Gent's Comment Blog # 6: Bought 50 SLRA at $24.45. I allowed the issuer to redeem my position at par plus accrued and unpaid interest which occurred in 1 partial call and than a full call.

Solar Capital Ltd. to Redeem Remaining $75 Million of 6.75% Senior Unsecured Notes due 2042; Increases Expected 2018 Net Investment Income by $0.04 Per Share; Prospectus Supplement

That bond was replaced with a $1K par value 4.5% senior unsecured bond maturing in 2023: Solar Capital Ltd. Prices Public Offering of $75 Million 4.50% Notes Due 2023

3. Short Term Bond/CD Ladder Basket Strategy:

August 2018 Maturities

SU = Senior Unsecured Bond

MI = Monthly Interest Payments

2 Wells Fargo 1.4% CDs MI 8/1/18 (18 Month CD)

2 Southeast Bank 1.8% CDs 8/8/18 (2 month CD)

2 Southeast Bank 1.8% CDs 8/8/18 (2 month CD)

2 Live Oak 1.65% CDs MI 8/9 (6 Month CD)

1 Deere 1.75% SU 8/10 (bought 2/15/18)

2 Lakeside Bank 1.4% CDs MI 8/13 (10 Month CD)

2 Whitney Bank 1.7% CDs 8/14 (6 Month CD)

1 Treasury 1% 8/15

1 First N.A. 1.6% CD MI 8/15 (6 Month)

2 Homestreet 1.7% CDs MI 8/16 (3 Month)

2 Goldman Sachs BK 1.5% CDs 8/16 (1 Year CDs)

4 Wells Fargo 1.5% CDs MI 8/20 (1 Year CDs)

1 Bank of West 1.45% CD 8/21 (9 Month CD)

2 Seacoast Bank 1.45% CDs MI 8/23 (1 Year CDs)

2 Compass Bank 1.45% CDs 9/24 (9 Month CDs)

1 Santander U.K. 2% SU 8/24 (bought December 2016)

2 Bank of Montreal 1.35% SU 8/28 (bought January 2018)

2 Pacific Premier 1.4% CDs MI 8/29 (9 Month CDs)

1 Goldman Sachs 1.45% CD 8/29 (9 month CD)

2 Bank of India 1.8% CDs 8/29 (1 month CD)

2 Bank of India 1.8% CDs 8/29 (1 month CD)

1 Compass BK 1.5% CD 8/30 (9 month CD)

2 Citizens BK 1.8% CDs 8/30 (3 month CDs)

2 Citizens BK 1.8% CDs 8/30 (3 month CDs)

2 Pinnacle BK 1.4% CDs MI 8/30/18 (1 Year CDs)

4 Treasury 1.5% 8/31

Total = $43K

I am not sure how I am going to redeploy the proceeds from those maturing bonds and CDs. Pending a decision on redeployment, I have slowed down my purchases of short term fixed coupon securities.

CD and treasury bill rates for the next 6 to 9 months are not attractive in light of rising inflation.

For 2019, I will reduce the average monthly dollar amounts received from maturing bonds and CDs from $40K to $50K to $30K to $40K

For the maturing Schwab CDs, I am leaning toward buying short term corporate bonds in 10 bond lots. I have to buy 10 at that broker to receive a $1 per bond commission.

Since my Schwab commission free trades will expire in a few days, I am not likely to buy commissionable stock exchange traded securities using that broker since I have an abundance of free trades at Fidelity and IB charges $1 for $100 shares vs. Schwab at $4.95.

Schwab does offer a variety of commission free ETFs to all of its customers.

A. Bought 2 Legg Mason 2.7% SU Bonds Maturing on 7/15/19:

This bond just made its semi-annual interest payment so the accrued interest payable to the seller was just $.75.

FINRA Page: Bond Detail (prospectus linked)

Issuer: Legg Mason Inc. (LM)

LM Analyst Estimates

LM SEC Filings

LM Annual Report

LM Earnings Report for the Q/E 3/31/18

Credit Ratings:

Bought at a Total Cost of 99.962

YTM at TC Then at 2.739%

Current Yield at TC = 2.701%

The one year treasury bill closed at on the day of purchase. Daily Treasury Yield Curve Rates

B. Bought 1 Treasury 1.375% Coupon Maturing on 9/30/19:

YTM: 2.45%

C. Bought 1 BP Capital 2.237% SU Bond Maturing on 5/10/19:

The market for BP Capital bonds frequently allows for 1 bond trades at either the best offer/ask price or close to it.

Finra Page: Bond Detail (prospectus linked)

Credit Ratings:

Moody's at A1

Fitch Affirms BP/BP Capital Markets at 'A'; Outlook Stable (5/24/18)

Issuer: Wholly owned subsidiary of BP PLC who guarantees the notes

BP Analyst Estimates

BP Analyst Estimates

Bought at a Total Cost of 99.887

YTM at TC Then at 2.38%

Current Yield at TC = 2.2395%

Fidelity CD Rates With May 2018 Maturities as of 7/23/18:

4. Small Ball:

A. Sold 10 ONB at $19.66:

Quote: Old National Bancorp (ONB)

Profit Snapshot: $29.18

Item # 1.B. Bought 10 ONB at $16.75 (2/15/18 Post)

Closing Price Last Friday: ONB $19.475 -$0.275 -1.39%

Dividend: Quarterly at $.13 per share

Old National Bank Dividend History

Dividend History: Viewed Negatively (the quarterly rate was slashed from $.23 to $.07 in 2009 and the raises since that time are still $.10 below the quarterly rate paid in the 2009 first quarter)

Last Earnings Report: Q/E 6/30/18

Old National reports 2nd quarter net income of $44.0 million, a 13.2% increase from a year ago

I discussed this earnings report in a prior comment.

ONB Trading Profits to Date: $786.29

Prior Discussions:

Item 2.A. Eliminated ONB-Sold 50 Shares at $18.55 (2/27/17 Post)(profit snapshot=$312.97)

Item # 2. Averaged Down: Bought 50 ONB at $12.25-Update For Regional Bank Basket As Of 1/19/16 - South Gent | Seeking Alpha

Item # 2. Bought 50 ONB at $13.1: Update For Regional Bank Basket Strategy As Of 1/6/16 - South Gent | Seeking Alpha

Item # 5. Bought in Roth IRA: 50 ONB at $11.38:Update For Regional Bank Basket Strategy As Of 1/28/16 - South Gent | Seeking Alpha

Comparative Data Charts at St. Louis Federal Reserve:

Disclaimer: I am not a financial advisor but simply an individual investor who has been managing my own money since I was a teenager. In this post, I am acting solely as a financial journalist focusing on my own investments. The information contained in this post is not intended to be a complete description or summary of all available data relevant to making an investment decision. Instead, I am merely expressing some of the reasons underlying the purchase or sell of securities. Nothing in this post is intended to constitute investment or legal advice or a recommendation to buy or to sell. All investors need to perform their own due diligence before making any financial decision which requires at a minimum reading original source material available at the SEC and elsewhere. A failure to perform due diligence only increases what I call "error creep". Stocks, Bonds & Politics: ERROR CREEP and the INVESTING PROCESS Each investor needs to assess a potential investment taking into account their personal risk tolerances, goals and situational risks. I can only make that kind of assessment for myself and family members.

I am not sure how I am going to redeploy the proceeds from those maturing bonds and CDs. Pending a decision on redeployment, I have slowed down my purchases of short term fixed coupon securities.

CD and treasury bill rates for the next 6 to 9 months are not attractive in light of rising inflation.

For 2019, I will reduce the average monthly dollar amounts received from maturing bonds and CDs from $40K to $50K to $30K to $40K

For the maturing Schwab CDs, I am leaning toward buying short term corporate bonds in 10 bond lots. I have to buy 10 at that broker to receive a $1 per bond commission.

Since my Schwab commission free trades will expire in a few days, I am not likely to buy commissionable stock exchange traded securities using that broker since I have an abundance of free trades at Fidelity and IB charges $1 for $100 shares vs. Schwab at $4.95.

Schwab does offer a variety of commission free ETFs to all of its customers.

A. Bought 2 Legg Mason 2.7% SU Bonds Maturing on 7/15/19:

This bond just made its semi-annual interest payment so the accrued interest payable to the seller was just $.75.

FINRA Page: Bond Detail (prospectus linked)

Issuer: Legg Mason Inc. (LM)

LM Analyst Estimates

LM SEC Filings

LM Annual Report

LM Earnings Report for the Q/E 3/31/18

Credit Ratings:

Bought at a Total Cost of 99.962

YTM at TC Then at 2.739%

Current Yield at TC = 2.701%

The one year treasury bill closed at on the day of purchase. Daily Treasury Yield Curve Rates

B. Bought 1 Treasury 1.375% Coupon Maturing on 9/30/19:

YTM: 2.45%

C. Bought 1 BP Capital 2.237% SU Bond Maturing on 5/10/19:

The market for BP Capital bonds frequently allows for 1 bond trades at either the best offer/ask price or close to it.

Finra Page: Bond Detail (prospectus linked)

Credit Ratings:

Moody's at A1

Fitch Affirms BP/BP Capital Markets at 'A'; Outlook Stable (5/24/18)

Issuer: Wholly owned subsidiary of BP PLC who guarantees the notes

Bought at a Total Cost of 99.887

YTM at TC Then at 2.38%

Current Yield at TC = 2.2395%

Fidelity CD Rates With May 2018 Maturities as of 7/23/18:

4. Small Ball:

A. Sold 10 ONB at $19.66:

Quote: Old National Bancorp (ONB)

Profit Snapshot: $29.18

Item # 1.B. Bought 10 ONB at $16.75 (2/15/18 Post)

Closing Price Last Friday: ONB $19.475 -$0.275 -1.39%

Dividend: Quarterly at $.13 per share

Old National Bank Dividend History

Dividend History: Viewed Negatively (the quarterly rate was slashed from $.23 to $.07 in 2009 and the raises since that time are still $.10 below the quarterly rate paid in the 2009 first quarter)

Last Earnings Report: Q/E 6/30/18

Old National reports 2nd quarter net income of $44.0 million, a 13.2% increase from a year ago

I discussed this earnings report in a prior comment.

ONB Trading Profits to Date: $786.29

Prior Discussions:

Item 2.A. Eliminated ONB-Sold 50 Shares at $18.55 (2/27/17 Post)(profit snapshot=$312.97)

Item # 2. Averaged Down: Bought 50 ONB at $12.25-Update For Regional Bank Basket As Of 1/19/16 - South Gent | Seeking Alpha

Item # 2. Bought 50 ONB at $13.1: Update For Regional Bank Basket Strategy As Of 1/6/16 - South Gent | Seeking Alpha

Item # 5. Bought in Roth IRA: 50 ONB at $11.38:Update For Regional Bank Basket Strategy As Of 1/28/16 - South Gent | Seeking Alpha

Item # 1 SOLD 100 ONB at $13 (8/22/12 Post)(snapshot of profit=$99.07)-Item # 4 Bought 100 ONB at $11.85 (5/29/2012 Post)

Item # 1 Sold 50 ONB at $14.12 (7/16/13 Post)(Profit snapshot=$95.13)-Item # 4 Bought Back 50 ONB at $11.9 (5/6/13 Post)

Net Interest Margin for all U.S. Banks (abbreviated to "NIM")

Return on Average Equity for all U.S. Banks (abbreviated to "ROE")

Return on Average Assets for all U.S. Banks (abbreviated to "ROA")

Nonperforming Loans (past due 90+ days plus nonaccrual) to Total Loans for all U.S. Banks (abbreviated to "NPL Ratio")

Net Percentage of Domestic Banks Tightening Standards for Commercial and Industrial Loans to Small Firms-St. Louis Fed

B. Bought 10 AT & T at $30.17-Used Commission Free Trade:

Closing Price Day of Trade (7/25/18): T $30.25 -1.43 -4.51%

Closing Price Last Friday (7/27): T $31.08 +$0.73 +2.41%

Investors reacted negatively to the earnings report released on 7/24 which is understandable though probably an overreaction. The non-Time Warner businesses, particularly the Direct TV entertainment division, are having issues. The stock established a new 52 week low at $30.13 on 7/24 with 96.358+M shares traded, well above the average volume of 44.144M shares.

Current Position: 52 shares

Average Cost Per Share = $32.69

Purchase Restriction: Small Ball Rule (currently averaging down in 10 share lots; each purchase has to be at the lowest price in the chain)

Dividend Yield at Total Average Cost = 6.12%

AT&T Historical Dividends

Dividend Reinvestment: Yes at below $35

On the bright side, sort of, the next dividend payment which will occur on 8/1/18 will be at a low price.

Chart: Major Bear Pattern

Recent Substantive Discussion: Item # 1.B. Bought 5 AT & T at $31.14 (7/25/18 Post)

I have nothing further to add to that recent discussion.

B. Bought 10 AT & T at $30.17-Used Commission Free Trade:

Closing Price Day of Trade (7/25/18): T $30.25 -1.43 -4.51%

Closing Price Last Friday (7/27): T $31.08 +$0.73 +2.41%

Investors reacted negatively to the earnings report released on 7/24 which is understandable though probably an overreaction. The non-Time Warner businesses, particularly the Direct TV entertainment division, are having issues. The stock established a new 52 week low at $30.13 on 7/24 with 96.358+M shares traded, well above the average volume of 44.144M shares.

Current Position: 52 shares

Average Cost Per Share = $32.69

Purchase Restriction: Small Ball Rule (currently averaging down in 10 share lots; each purchase has to be at the lowest price in the chain)

Dividend Yield at Total Average Cost = 6.12%

AT&T Historical Dividends

Dividend Reinvestment: Yes at below $35

On the bright side, sort of, the next dividend payment which will occur on 8/1/18 will be at a low price.

Chart: Major Bear Pattern

Recent Substantive Discussion: Item # 1.B. Bought 5 AT & T at $31.14 (7/25/18 Post)

I have nothing further to add to that recent discussion.